Why Understanding Interest Rates Helps Borrowers Make Better Financial Decisions

When individuals begin exploring personal loan options, one of the most important factors to understand is the interest rate. Interest plays a significant role in determining the total cost of borrowing, the affordability of monthly payments, and the overall financial impact over time. At Portside Finance, we believe borrowers make stronger and more confident financial choices when they understand how interest rates work and how these rates influence their long term budgets. Clear knowledge empowers individuals to evaluate loan offers accurately and select options that support their financial well being.

What Interest Rates Represent

An interest rate reflects the cost of borrowing money. It is the amount a borrower pays in addition to the principal balance throughout the life of the loan. Lenders evaluate several factors when determining interest rates, including income stability, credit score, loan type, and repayment terms. When borrowers understand what these rates represent, they can better assess how each loan will affect their finances.

An interest rate is not simply a number printed on a loan agreement. It is a direct indicator of the total amount that will be repaid and a key component of the monthly payment structure. Even small differences in interest rates can affect repayment amounts and the overall cost of the loan.

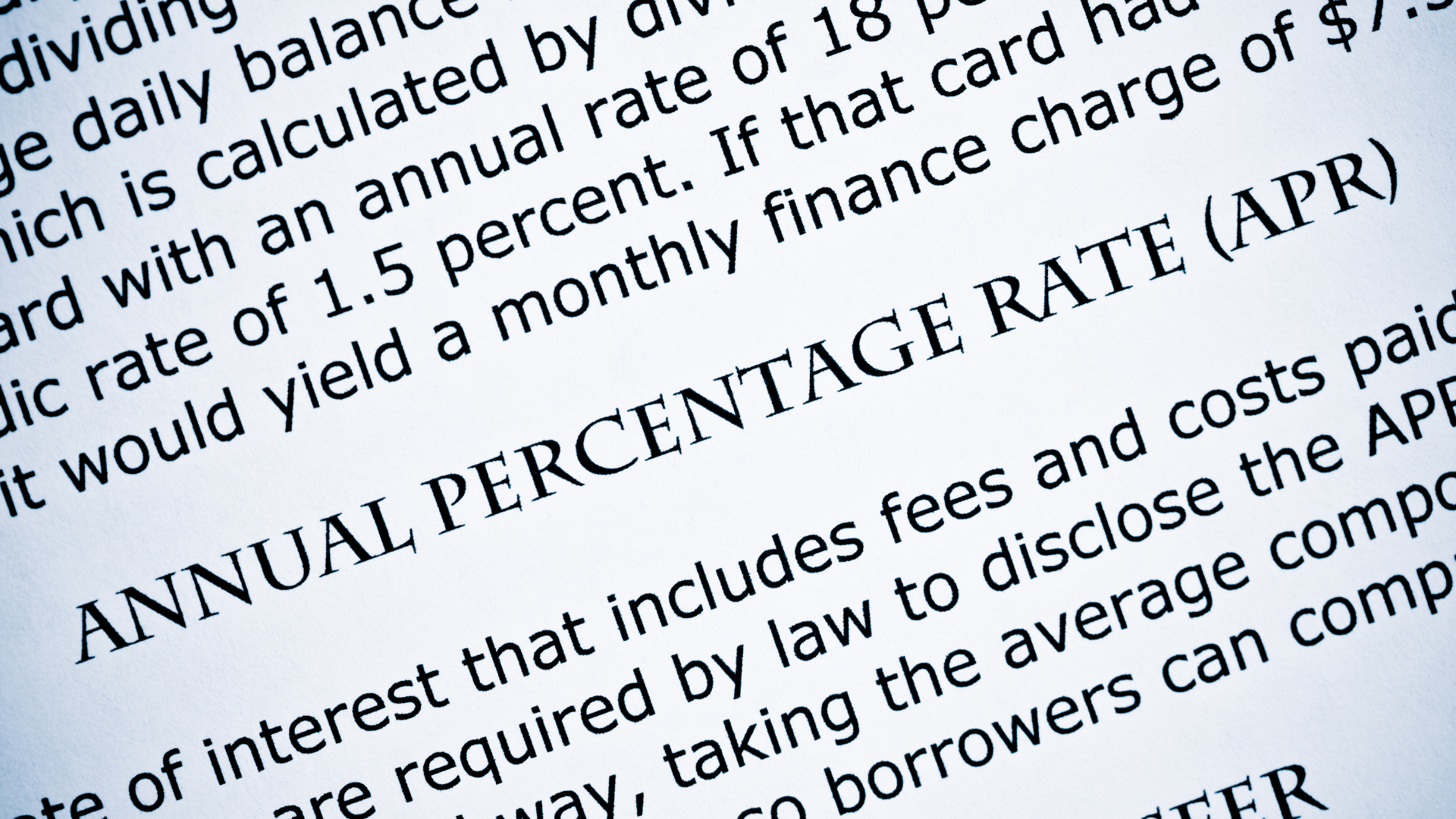

Why APR Matters

Borrowers often see two different numbers when reviewing loan options. The interest rate indicates the basic cost of borrowing, while the Annual Percentage Rate, or APR, includes additional fees or charges associated with the loan. APR provides a more complete picture of the true borrowing cost.

Understanding APR helps borrowers compare loan offers more accurately. A loan with a slightly lower interest rate but higher fees may be more expensive than another loan with a higher interest rate and fewer additional costs. By reviewing the APR, borrowers gain clarity and avoid selecting a loan that appears affordable at first glance but becomes more costly over time.

Fixed Rates Provide Predictability

Many personal loans feature fixed interest rates. A fixed rate remains stable throughout the life of the loan, which helps borrowers plan long term budgets with confidence. With predictable monthly payments, individuals can manage their income and expenses without worrying about sudden increases.

This stability can be especially beneficial for individuals who are rebuilding credit or managing tight budgets, since predictable payments reduce the risk of financial strain. Fixed rates provide structure, consistency, and peace of mind for borrowers who value dependable repayment schedules.

How Credit Scores Influence Rates

Credit scores play a central role in determining interest rates. A strong credit score signals responsible financial behavior, while a lower score may indicate missed payments or high debt levels. Individuals with higher credit scores often receive lower interest rates because lenders view them as lower risk.

This relationship highlights why credit monitoring and responsible financial habits are essential. By making consistent payments, reducing outstanding debt, and avoiding excessive credit inquiries, borrowers can improve their credit profiles over time. Stronger credit may lead to improved loan terms and lower interest costs in the future.

Evaluating Affordability Before Borrowing

Understanding interest rates helps borrowers realistically evaluate whether a particular loan is affordable. When reviewing loan options, individuals should consider both the monthly payment and the total repayment amount. A loan with a lower monthly payment may have a longer term, which increases the total interest paid over time.

Borrowers benefit from taking a full view of their financial commitments, including rent or mortgage payments, utilities, groceries, and other recurring expenses. When individuals select a loan that aligns comfortably with their budget, they reduce the risk of late payments or financial pressure.

How Knowledge Supports Responsible Borrowing

Interest rate awareness encourages responsible borrowing. Borrowers who understand how interest accrues are more likely to compare offers, read loan terms carefully, and make decisions that support their long term financial goals. This knowledge also helps individuals recognize when a loan will provide constructive financial support versus when it may lead to unnecessary strain.

At Portside Finance, we encourage all borrowers to ask questions, review terms thoroughly, and prioritize clarity before signing any agreement. Our team is committed to helping individuals understand the factors that influence interest rates so they can make informed decisions confidently.

Building Financial Confidence Through Understanding

Interest rates are a significant part of the borrowing process, and understanding them is essential for long term financial stability. When individuals know how rates are determined, how they affect monthly payments, and how they contribute to total loan costs, they gain the tools needed to borrow responsibly. Through clear information and supportive guidance, we help our clients make financial decisions that align with their goals and strengthen their financial confidence.