How to Prepare Financially Before Applying for Your First Loan

Applying for your first loan can feel overwhelming. Many first time borrowers are unsure what lenders look for or how to present themselves as strong applicants. Preparation makes a meaningful difference. Taking time to review your financial situation before applying can help you borrow more confidently and responsibly. At Portside Finance, we believe informed borrowers are better positioned for long term financial success.

Understand Why You Need the Loan

Before completing an application, it is important to clearly define the purpose of the loan. First time borrowers should ask whether the loan is addressing a short term need, helping manage cash flow, or supporting a specific financial goal. Being clear about intent helps guide decisions about loan size and repayment terms.

Borrowing without a defined purpose can lead to unnecessary stress. A well considered plan supports responsible use of credit and improves the overall borrowing experience.

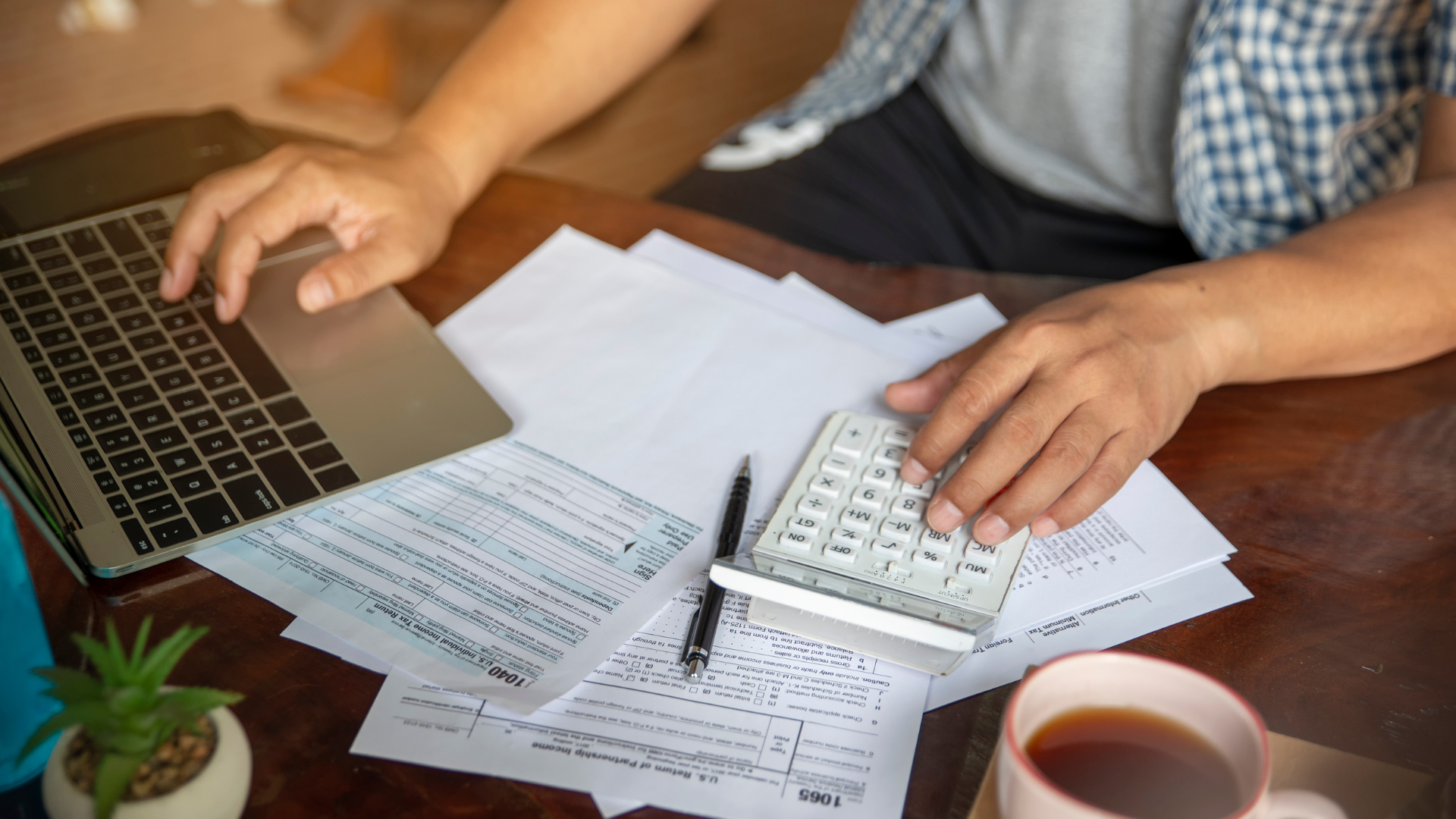

Review Your Income and Monthly Obligations

One of the first steps in preparation is understanding your income and expenses. Lenders evaluate whether a borrower can reasonably manage repayment. Reviewing pay stubs, bank statements, and recurring expenses provides a realistic picture of affordability.

First time borrowers should calculate how a loan payment fits into their existing budget. This includes rent or mortgage payments, utilities, transportation costs, and other obligations. Knowing these numbers in advance helps avoid borrowing more than necessary.

Check Your Credit Profile

Many first time borrowers assume they have no credit history, but that is not always the case. Student loans, credit cards, or utility accounts may already appear on a credit report. Reviewing your credit profile allows you to identify what lenders will see.

Checking for errors or outdated information is an important step. Even small inaccuracies can affect how an application is evaluated. Understanding your credit standing also helps set realistic expectations before applying.

Gather Required Documentation

Being organized speeds up the application process. Lenders typically require proof of income, identification, and banking information. Preparing these documents ahead of time reduces delays and frustration.

First time borrowers often feel more confident when they know what information will be requested. Having documentation ready demonstrates preparedness and helps the process move smoothly.

Consider the Type of Loan That Fits Your Situation

Not all loans are structured the same way. First time borrowers should understand whether a secured or unsecured loan best fits their needs. Secured loans may involve collateral, while unsecured loans rely more heavily on credit and income factors.

Understanding these differences helps borrowers make informed choices rather than applying blindly. Selecting the right type of loan supports responsible borrowing and manageable repayment.

Plan for Repayment From the Start

Preparing for a loan means planning for repayment before funds are received. First time borrowers should review payment schedules and consider how payments will be made. Automatic payments, due dates, and repayment timelines should align with income cycles.

Thinking about repayment early reduces the risk of missed payments. Consistent repayment supports financial stability and may contribute positively to credit history over time.

Ask Questions and Seek Clarity

First time borrowers should feel comfortable asking questions. Understanding loan terms, fees, and expectations is essential. No borrower benefits from uncertainty or assumptions.

At Portside Finance, we encourage open communication. Clear information helps borrowers feel confident and supported throughout the process.

Building Confidence Through Preparation

Preparing financially before applying for your first loan is about more than approval. It is about building confidence and establishing healthy borrowing habits. When borrowers understand their finances, choose appropriate loan options, and plan for repayment, they are better positioned for success.

At Portside Finance, we work with first time borrowers who want to approach borrowing thoughtfully. Preparation is the first step toward responsible credit use and long term financial confidence.